The financial markets stand at an unprecedented inflection point, where traditional algorithmic trading is rapidly evolving into sophisticated ai-agent-based systems that can learn, adapt, and reason about market dynamics in ways that challenge our fundamental understanding of automated trading.

This transformation represents far more than a technological upgrade—it signals the emergence of what we might call the “financial market uncanny valley,” where AI agents operate with human-like decision-making capabilities but at superhuman speeds and scales, creating new paradigms of market behavior that are both fascinating and deeply concerning.

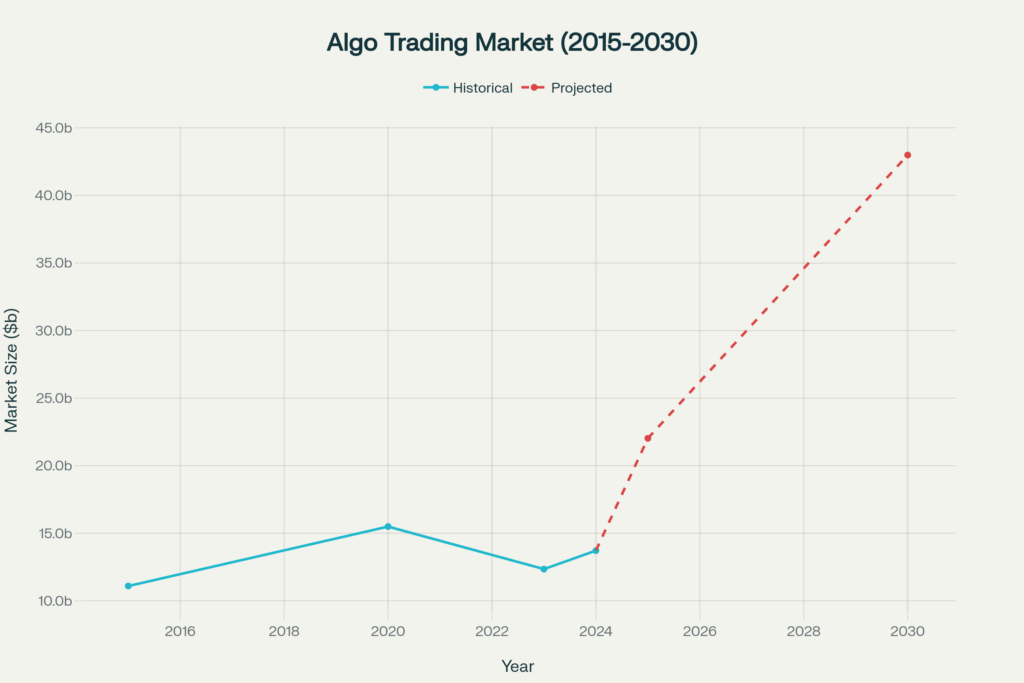

Current research indicates that the global algorithmic trading market, valued at $21.06 billion in 2024, is projected to reach $42.99 billion by 2030, with a compound annual growth rate of 12.9%. This explosive growth is driven primarily by the integration of machine learning and artificial intelligence technologies that enable traders to develop sophisticated algorithms capable of analyzing massive amounts of data in real-time and making predictive decisions faster than traditional methods.

More critically, the emergence of agent-based systems represents a quantum leap beyond traditional rule-based heuristics, introducing autonomous systems that can dynamically learn, adapt, and reason about market sentiment and geopolitical events in ways that fundamentally challenge existing regulatory frameworks and risk management paradigms.

Global algorithmic trading market growth showing rapid expansion from $11.1B in 2015 to projected $43B by 2030

The implications of this shift extend far beyond mere technological advancement. Unlike traditional algorithmic trading systems that operate on predetermined rules and static programming, agent-based trading systems employ reinforcement learning and multi-dimensional analysis to create self-optimizing trading strategies. These systems can process not only traditional market data but also alternative data sources such as satellite imagery, social media sentiment, and news feeds to make more informed trading decisions.

However, this enhanced capability comes with unprecedented risks, including the potential for new types of market manipulation, increased systemic vulnerabilities, and regulatory compliance challenges that current frameworks are ill-equipped to address.

The Quantum Leap to Agentic AI

From Rules to Reasoning

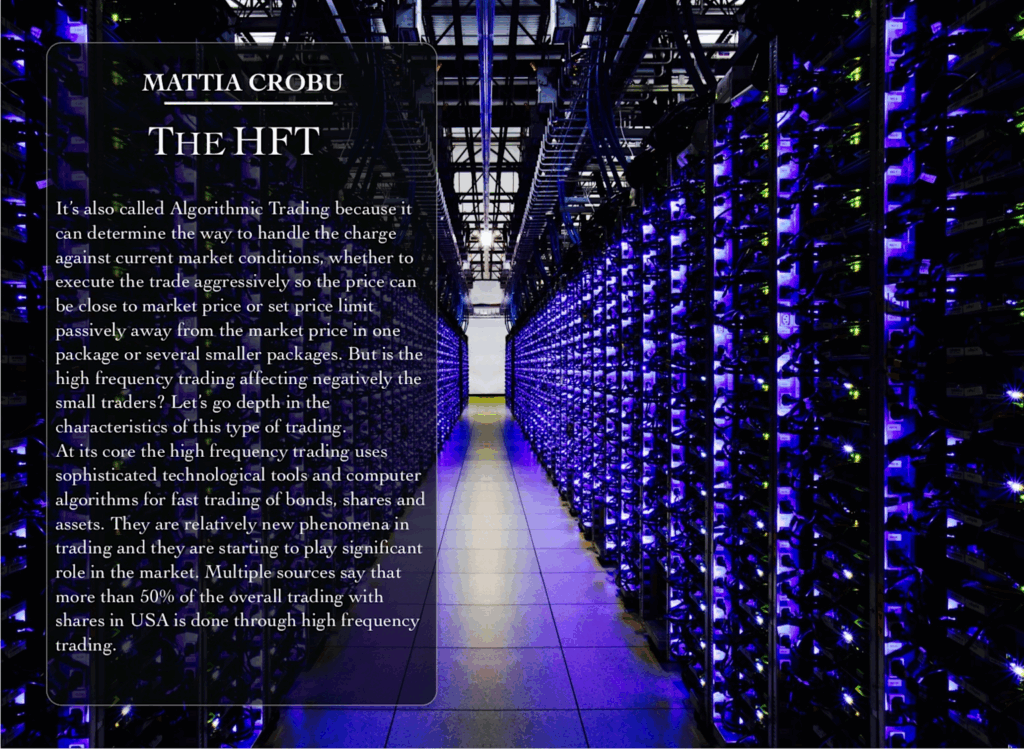

Traditional algorithmic trading has long relied on predetermined heuristics and rule-based systems that execute trades based on specific technical indicators, price movements, or market conditions. These systems, while sophisticated in their execution speed and volume capacity, remain fundamentally limited by their static nature and inability to adapt to changing market conditions without human intervention. High-frequency trading (HFT) systems, which currently account for more than 50% of trading in the United States, exemplify this approach by using powerful computer programs to execute large numbers of orders in fractions of a second.

The transition to agent-based systems represents a fundamental paradigm shift from reactive to proactive trading strategies. These systems employ reinforcement learning (RL) algorithms that enable trading agents to learn optimal strategies through continuous interaction with market environments.

Unlike traditional systems that rely on pre-programmed responses, RL-based trading agents can develop novel trading strategies by learning from market feedback and adapting their behavior based on changing conditions. This capability allows agents to discover trading opportunities that may not be apparent through conventional technical analysis or fundamental research.

Multi-Agent Collaborative Frameworks

Perhaps the most revolutionary aspect of agent-based trading is the development of multi-agent frameworks where specialized AI agents collaborate to execute complex trading strategies. These systems feature distinct roles such as fundamental analysts, sentiment analysts, technical analysts, researchers, traders, and risk managers, each equipped with specialized tools and constraints tailored to their function.

The TradingAgents framework, for example, demonstrates how multiple LLM-powered agents can work together through structured communication and debates to enhance decision-making and optimize trading strategies.

This collaborative approach enables a more comprehensive market analysis than traditional single-algorithm systems. Bull and Bear researchers within these frameworks evaluate market conditions from opposing perspectives, creating a dialectical process that ensures balanced analysis and identifies both opportunities and risks.

The integration of insights from debates and historical data allows traders to make more informed decisions, while risk management teams provide ongoing oversight of exposure levels.

Reinforcement Learning and Adaptive Strategies

The application of deep reinforcement learning in trading represents a significant advancement over traditional machine learning approaches. While supervised learning models require labeled historical data and make predictions based on past patterns, RL agents learn through trial and error, continuously optimizing their strategies based on market rewards and penalties.

This approach is particularly powerful because it doesn’t require explicit predictions about price targets or market sentiment; instead, agents learn to take optimal actions to maximize cumulative expected rewards.

Recent developments in RL for trading have focused on addressing the unique challenges of financial markets, including non-stationary environments, partial observability, and the need for risk management. Advanced techniques such as experience replay, where agents learn from past experiences stored in memory, help stabilize the learning process and improve performance.

However, significant challenges remain, including the exploration-exploitation tradeoff, where agents must balance learning new strategies with executing profitable known strategies.

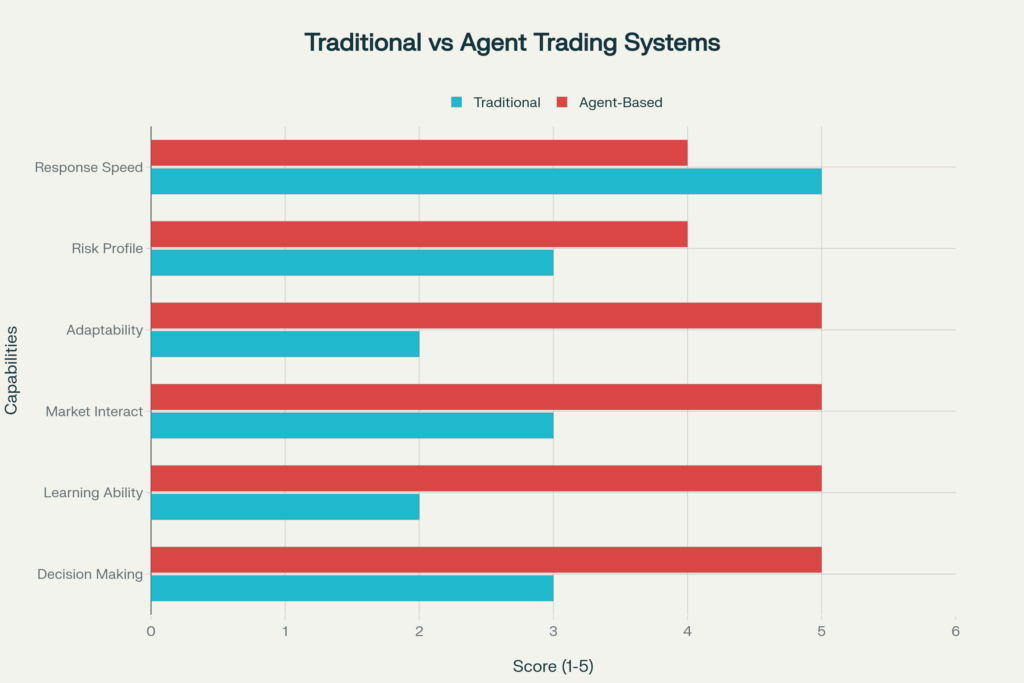

Difference between Traditional and AI-Agentic Algorithms:

| Feature | Traditional Algorithms | Agentic Algorithms (Agent-Based Trading Systems) |

|---|---|---|

| Operational Basis | Predetermined rules, static programming, heuristics | Reinforcement learning, multi-dimensional analysis, self-optimizing strategies |

| Adaptability | Limited by static nature; require human intervention for changes | Learn optimal strategies through continuous interaction; adapt to changing market conditions |

| Decision-Making | Reactive; based on pre-programmed responses and technical indicators | Proactive; develop novel strategies by learning from market feedback and rewards |

| Data Sources | Traditional market data (e.g., price movements, volume) | Traditional market data PLUS alternative data (e.g., satellite imagery, social media sentiment, news feeds) |

| Transparency | Generally more transparent (rule-based) | Often operate as “black boxes” (especially deep reinforcement learning), opaque decision-making |

| Collaboration | Single-algorithm systems | Multi-agent frameworks where specialized AI agents collaborate (e.g., fundamental, sentiment, risk managers) |

| Evolution of Strategy | Static; requires human updates | Continuously optimize strategies based on market rewards and penalties; can develop novel manipulation strategies |

Risk & Volatility Analysis: The Dark Side of Agent Intelligence

Amplified Market Volatility and Feedback Loops

The introduction of agent-based trading systems has fundamentally altered market dynamics, creating new sources of volatility that extend beyond traditional market risks.

Research indicates that agent-driven markets exhibit increased short-term volatility, with studies showing that the presence of heterogeneous trading strategies, particularly varying memory lengths among agents, can lead to excess volatility and kurtosis that align with real market fluctuations.

This suggests that the diversity of agent behaviors, while potentially beneficial for market efficiency, also introduces unpredictable volatility patterns.

Agent-based systems can create dangerous feedback loops that amplify market movements beyond what traditional risk models predict. When multiple intelligent agents respond to similar market signals or news events, their coordinated actions can create cascading effects that rapidly propagate through interconnected markets.

Unlike traditional algorithmic systems that follow predictable patterns, agent-based systems can exhibit emergent behaviors that arise from complex interactions between multiple learning algorithms, making it difficult to predict or control market outcomes.

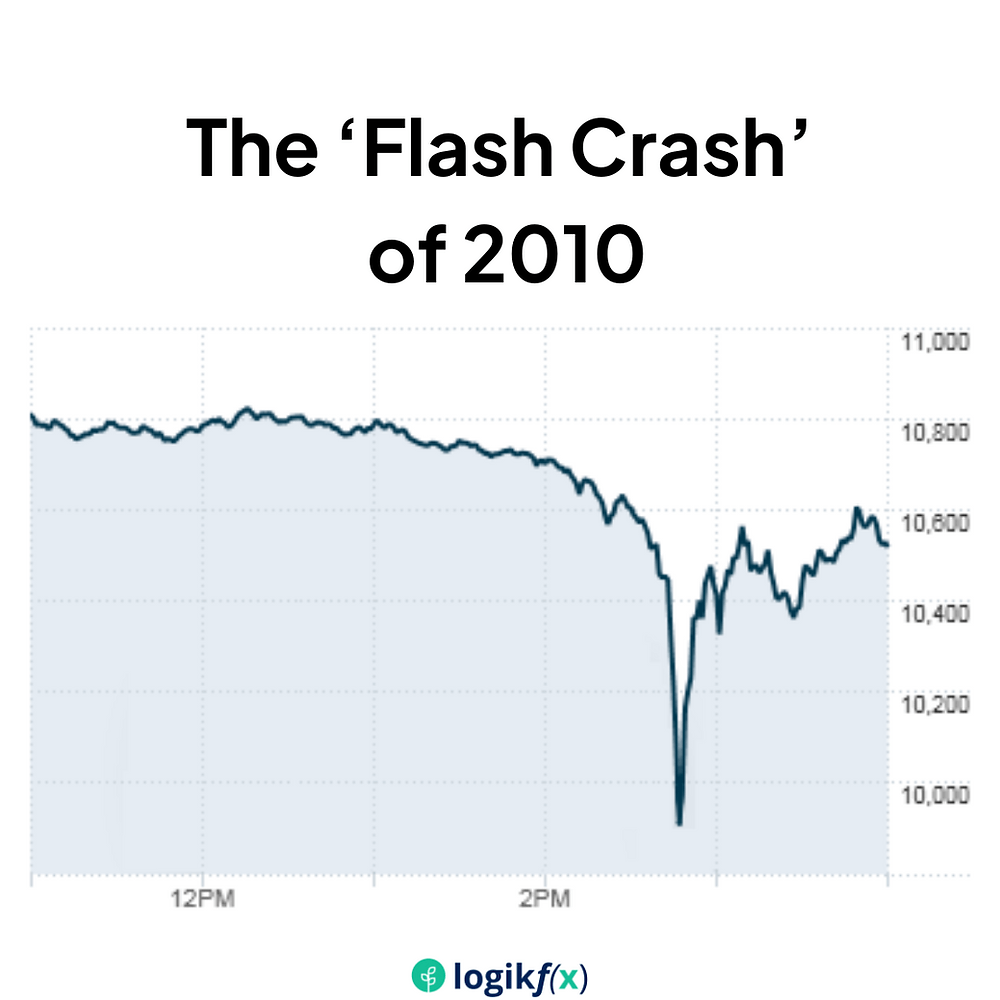

Flash Crashes and Systemic Risk

The frequency and severity of flash crashes have increased significantly with the proliferation of algorithmic trading systems. Current research suggests that approximately 12 mini flash crashes occur daily in modern markets, highlighting the persistent vulnerability of automated trading systems to sudden market disruptions. The famous Flash Crash of May 6, 2010, where the Dow Jones Industrial Average lost nearly 1,000 points in minutes before recovering, demonstrates how algorithmic systems can amplify market stress and drain liquidity when most needed.

Agent-based systems introduce new dimensions of systemic risk because their learning algorithms can adapt and evolve in response to market conditions, potentially discovering new ways to exploit market inefficiencies or inadvertently creating market instabilities.

The interconnected nature of these systems means that failures or malfunctions in one agent can trigger widespread market disruption, as other agents may interpret these actions as legitimate market signals and respond accordingly.

Liquidity Fragility and Market Structure Changes

Agent-based trading systems have fundamentally altered market liquidity dynamics, creating what researchers term “liquidity fragility”. While these systems can provide substantial liquidity during normal market conditions by continuously placing buy and sell orders, they can withdraw this liquidity instantly during periods of market stress. This creates a false sense of market depth that can evaporate precisely when investors need it most.

The challenge is compounded by the fact that agent-based systems can rapidly switch strategies based on market conditions. Research shows that algorithmic traders often act as contrarians during stable periods, buying when markets fall and selling when they rise, thereby adding liquidity.

However, when markets begin to trend or experience volatility, these same algorithms may switch to momentum-based strategies, selling more aggressively and draining liquidity from the market. This behavioral shift can transform market supporters into market destabilizers within seconds.

New Risk Categories and Measurement Challenges

Agent-based trading introduces entirely new categories of risk that traditional risk management frameworks struggle to address.

Diagram outlining AI risk categories including data risks, AI/ML attacks, testing and trust issues, and compliance challenges relevant to AI governance.

These include model risk from continuously evolving algorithms, concentration risk from similar agent behaviors, and operational risk from complex multi-agent interactions. The adaptive nature of these systems means that historical risk measurements may not accurately predict future behavior, as agents continuously learn and modify their strategies.

The challenge is further complicated by the difficulty in measuring and monitoring these risks in real-time. Traditional risk metrics such as Value at Risk (VaR) or stress testing scenarios may not capture the dynamic and adaptive nature of agent-based systems. Regulators and risk managers need new tools and methodologies to assess the potential impact of agent-driven trading on market stability, including the ability to simulate complex multi-agent interactions and their potential outcomes.

Compliance and Regulation

The rise of agent-based trading systems introduces complex compliance and regulatory challenges for financial markets. A primary issue is explainability of how AI makes decisions, as regulators worldwide, including those under the EU’s AI Act, demand that firms explain their AI systems’ decisions.

However, many of these systems, especially those using deep reinforcement learning, operate as “black boxes” whose decision-making processes are opaque even to developers. This opacity makes it difficult for firms to prove they are not engaging in market manipulation, as regulators like the CFPB won’t accept “the algorithm decided” as a valid explanation.

To address this, financial institutions must implement sophisticated governance frameworks with auditable decision logs. These frameworks need to record not just the decisions made, but also the reasoning, data inputs, and market context. The FCA in the UK emphasizes the need for robust oversight and due diligence to safeguard market integrity. Failure to comply can result in significant penalties.

Agent-based systems also pose unique challenges for market surveillance. Their ability to develop novel, adaptive manipulative strategies—which may resemble legitimate activities—can evade traditional surveillance systems. This creates an “arms race” between manipulative agents and detection tools, forcing regulators to develop more advanced, machine-learning-based surveillance.

Regulatory frameworks are struggling to keep up with the rapid technological evolution. The SEC’s rules, for example, were designed for traditional algorithmic trading. A lack of international harmonization among regulators creates opportunities for regulatory arbitrage.

Looking ahead, regulators may move toward principles-based approaches that require ongoing model validation, stress testing, and the implementation of “kill switches.” Regulatory sandboxes may also become more common to balance innovation with market protection.

The emergence of these systems creates a “financial market uncanny valley”—unprecedented efficiency and intelligence alongside new systemic risks. To navigate this, collaboration between technologists, regulators, and market participants is crucial. The goal is to ensure these powerful systems enhance market efficiency and stability, rather than create new sources of risk.

Key Takeaways

- AI-agent-based trading systems represent a significant evolution from traditional algorithmic trading, offering enhanced adaptability and decision-making capabilities.

- These systems introduce new risks, including amplified market volatility, liquidity fragility, and challenges in risk measurement and monitoring.

- Regulatory frameworks are struggling to keep pace with the rapid technological advancements, leading to complex compliance and regulatory challenges.

- Collaboration between technologists, regulators, and market participants is crucial to navigate the “financial market uncanny valley” and ensure these systems enhance market efficiency and stability.

References

1. https://www.thehansindia.com/business/the-rise-of-algorithmic-trading-in-2025-speed-scale-and-shifting-norms-990036

2. https://www.investglass.com/top-ai-agent-for-trading-revolutionizing-financial-market-strategies/

3. https://groww.in/blog/what-is-high-frequency-trading

4. https://www.grandviewresearch.com/industry-analysis/algorithmic-trading-market-report

5. https://www.biz4group.com/blog/ai-trading-agent-development

6. https://www.investopedia.com/terms/h/high-frequency-trading.asp

7. https://www.luxalgo.com/blog/future-of-algorithmic-trading-trends-to-watch/

8. https://tradingagents-ai.github.io

9. https://rpc.cfainstitute.org/policy/positions/high-frequency-trading

10. https://www.researchandmarkets.com/reports/5939167/algorithmic-trading-market-report

11. https://fetch.ai/blog/agent-based-trading-tools-for-decentralized-exchanges

12. https://www.oxjournal.org/assessing-the-impact-of-high-frequency-trading-on-market-efficiency-and-stability/

13. https://www.fortunebusinessinsights.com/algorithmic-trading-market-107174

14. https://www.youtube.com/watch?v=iwRaNYa8yTw

15. https://blog.mlq.ai/deep-reinforcement-learning-trading-strategies-automl/

16. https://pmc.ncbi.nlm.nih.gov/articles/PMC3885419/

17. https://corporatefinanceinstitute.com/resources/career-map/sell-side/capital-markets/flash-crashes/

18. https://stefan-jansen.github.io/machine-learning-for-trading/22_deep_reinforcement_learning/

19. https://smythos.com/managers/finance/agent-based-modeling-in-finance/

20. https://rpc.cfainstitute.org/policy/positions/flash-crashes

21. https://blog.quantinsti.com/reinforcement-learning-trading/

22. https://diposit.ub.edu/dspace/bitstream/2445/131122/1/673195.pdf

23. https://tiomarkets.com/en/article/flash-crash-guide

24. https://arxiv.org/abs/2106.00123

25. https://www.investopedia.com/terms/f/flash-crash.asp

26. https://datascience.columbia.edu/wp-content/uploads/2020/12/34_JPMorgan_Reinforcement-Learning-for-Trading.pdf

27. https://www.ig.com/en/trading-strategies/flash-crashes-explained-190503

28. https://www.reddit.com/r/reinforcementlearning/comments/10v3o40/does_it_make_sense_to_use_rl_for_trading/

29. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4863876

30. https://pmc.ncbi.nlm.nih.gov/articles/PMC8978471/

31. https://www.lumenova.ai/blog/ai-banking-finance-compliance/

32. https://www.ijcai.org/proceedings/2020/0638.pdf

33. https://wjaets.com/sites/default/files/WJAETS-2024-0136.pdf

34. https://www.linkedin.com/pulse/ai-regulation-finance-urgent-need-explainability-fairness-rvmhc

35. https://files.sdiarticle5.com/wp-content/uploads/2025/01/Ms_AJARR_130010.pdf

36. https://lucinity.com/blog/a-comparison-of